Scenarios: How Our Research Agent Thinks About What Could Happen

A news reader finishes a story and moves on. An analyst doesn't. They're running the next few weeks in their head — a few ways it could play out, what would have to be true for each, the version they don't want to believe. That stretch of quiet thinking is most of the job.

Most AI tools skip it entirely. We built ours to take it on purpose.

Why "What Happened" Isn't Enough

Fig 1: Forecasts under uncertainty start by drawing the branches.

Today's assistants are good at one thing: telling you what already happened. Ask about Tesla's last earnings call, and you'll get a clean summary. That's useful, but only a small fraction of what an analyst does.

The questions that land on a portfolio manager's desk are rarely about the past:

- If oil stays above $90 for another quarter, who in this basket starts to hurt?

- What does the risk path look like if the regulator wins?

- Where could this story go from here — and which version would catch us off guard?

Those aren't lookups. They are forecasts under uncertainty. Faced with one, most models either refuse to answer or invent one with false confidence.

A Step That Earns Its Speculation

Our agent has a step we call simulation, and it only runs when the question asks for it. A backward-looking question gets the facts and stops. Anything that touches outlook, exposure, or risk triggers it.

When it runs, it fills in four things, in order:

- Two to four scenarios. Each with a name, a trigger, a short narrative, what it would mean for the companies in play, and a probability label — low, medium, or high. The labels matter. They force a position.

- A risks list. Not a disclaimer — an actual list. What could go wrong, how badly, and which piece of evidence points there.

- A few judgements. Where the evidence supports a direction, the agent says so, and says how confident. Where it doesn't, it stays quiet.

- Considerations. Caveats and second-order effects to keep in mind while reading the rest.

This shape exists because "forward-looking" goes wrong in two predictable ways. It gets vague — everything is possible, nothing is said. Or it overcommits — here is the future, take it. The four-part format closes both corners.

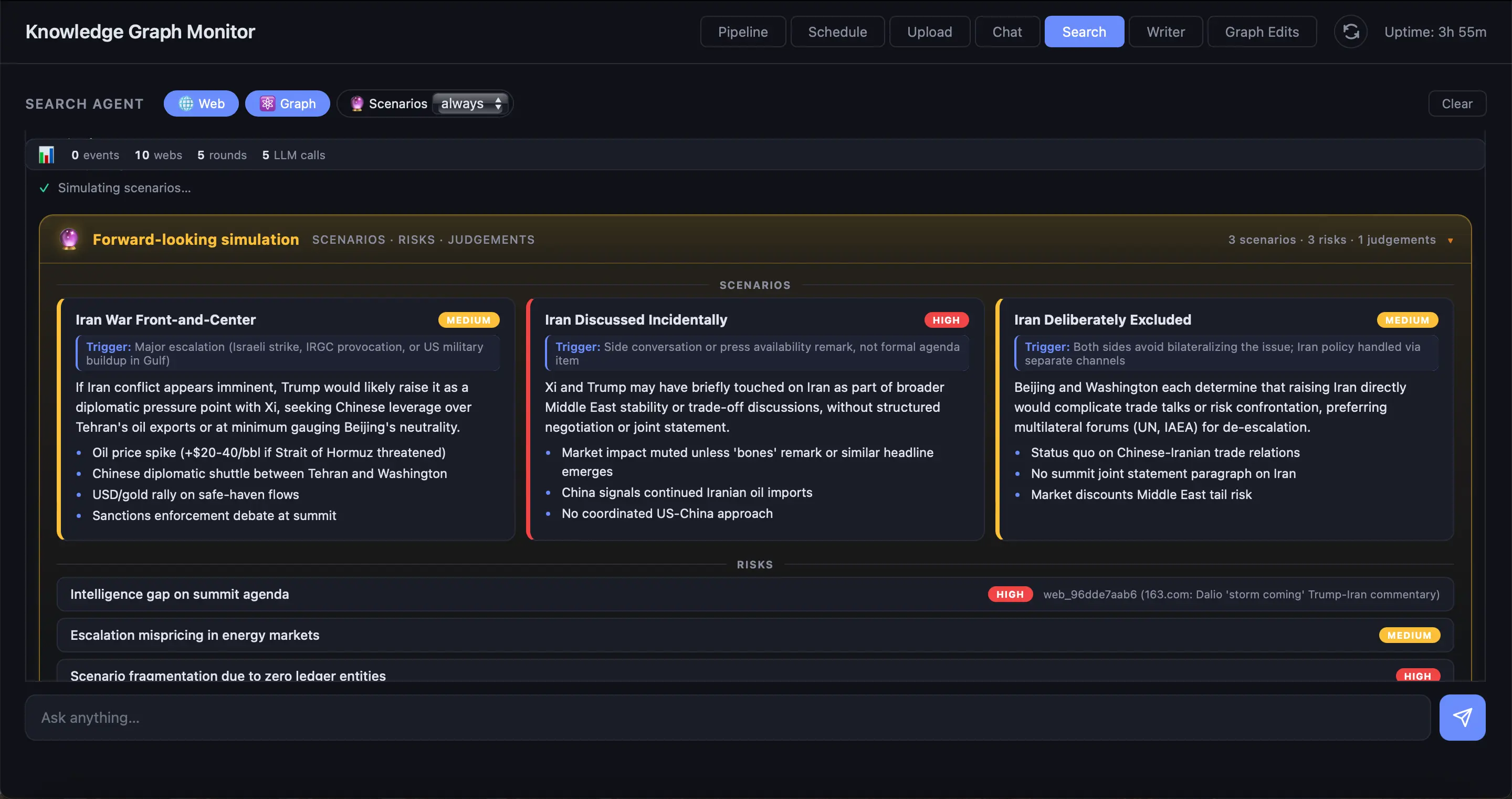

Fig 2: Screentshot for a scenario example based on Trump-Xi meeting.

Grounded, Not Imagined

What matters most isn't the output — it's what the model is allowed to draw from. The simulation step can't invent companies, supply-chain links, or events that aren't already in the record. Everything it reasons over was pulled from our knowledge graph and live web evidence in earlier steps. Real entities, real relationships, real recent events. That is the only material on the table.

Without that rule, "what could happen?" is creative writing. With it, it's research.

Where It Sits in the Bigger Picture

Simulation is one step in a longer process, not the whole pipeline. Before it runs, the agent has already built up a picture of what's known, reconciled the places where sources disagree, and figured out what it can defend. Only then — and only if the question warrants it — does the simulation step pick up the pen. Everything gets woven into one answer at the end, with citations.

The order matters: by the time we get to futures, the present is already pinned down. The forward-looking part of an answer reads like the next paragraph, not a separate appendix.

Revisable, Not Fixed

Fig 3: Ask again next week, the branches move with the evidence.

Two things follow from how the agent gets its evidence.

First, every scenario it produces is an if-then, not a forecast. It says: given what is true about these companies and relationships right now, here is a future the evidence supports. When the picture changes, the scenarios change. Ask the same question next week and you may get different futures, or different probability labels, because the market itself has moved.

Second, the simulation step gets sharper as the graph deepens. New filings come in. Guidance gets revised. Event chains extend. The agent's triggers tighten, the exposed entities get more specific, and paths that no longer make sense drop off. For an analyst, that turns simulation into something to revisit rather than a memo to file. The range of plausible futures is a moving object, and the agent moves with it.

A Note on Agent Swarms

A quick aside, since the question comes up. Another style of "simulation" is gaining attention, where the system creates a swarm of AI personas — buyers, regulators, voters — and lets them interact across dozens of rounds inside a synthetic world. The prediction is whatever the crowd settles on.

That works well when crowd dynamics are the point: marketing reactions, public opinion, viral spread. If the thing you're predicting is emergent behavior, you want a system that produces it.

But that is almost never the question on a portfolio manager's screen. Portfolio managers ask portfolio questions — what happens to this company, this sector, this exposure — and for those, a crowd is not what you need. You need the discipline analysts have used for decades: named scenarios, explicit triggers, ranked risks, stated confidence. We chose that approach deliberately.

One other thing. A simulator that runs on every query has to manufacture a future even for questions about the past. Ours stays out of the way until the question warrants it.

What This Unlocks

What you get is the difference between an answer and a starting point. A pure summary closes the conversation. A simulation opens one: here are the futures we think are live, here is what would have to be true for each, and here is what to watch to figure out which one we are actually in.

That is the conversation we built the agent for.

What's Coming Next

Simulation sits on top of FinCatch's financial world model and inherits everything we add to it. Richer events. Deeper coverage. Better tracking of how a development in one place propagates two or three steps away. Every addition to the graph shows up as sharper triggers, more specific exposure, and scenarios that fit a particular portfolio better than a generic one.

We're pushing the step further: longer event chains, faster reaction as new information arrives, scenarios shaped around an investor's actual thesis rather than a generic market view. More on that soon.